As a small and medium-sized enterprise (SME), and or entrepreneur, you’re well aware of how much time, effort and money it takes to win new business. Unfortunately, there’s always the threat of larger competitors coming in and stealing what you’ve worked so hard to close. So, should you resign yourself to this fate, or should you instead use a strategy to ensure that you not only keep your customers, but that you never lose another sale to a larger competitor again?

Answering that aforementioned question might involve offering consignment inventory agreements to your customers. These agreements allow you as the vendor to secure an incumbent position with your customers, while also guaranteeing you’ll keep their business long-term. You’ll ship a large volume of product to your customer’s location at the outset of the agreement. That customer will hold that inventory and provide you with weekly and or monthly updates on usage. Your customer is then invoiced according to the amount they used in that particular month. However, the inventory that remains is still owned by your company until it’s invoiced.

Customer Benefits of Consignment Inventory

Your customer benefits tremendously from these agreements because they never encounter a stock out, never have to incur expedite fees on rush orders, and never incur high freight costs for next day delivery. The inventory is there when they need it. In the end, it’s an excellent option for customers as it helps them reduce a substantial portion of their overall costs of inventory. However, what about your company’s position as the vendor in these types of agreements? What costs are involved in shipping product in advance and not generating an invoice until your customer provides a usage report?

Understanding Your Costs as a Vendor

Both you and your customer will benefit from this agreement. They have the inventory ready when needed, and your company secures an incumbent position. However, there are carrying costs your company still covers while that inventory remains at your customer’s location. These carrying costs are no different than if the inventory was still in your warehouse, waiting to be shipped. Here are some costs to consider and some things to discuss with your customer upfront.

1. Financing

Whatever remains unused by your customer must still be financed by your company. In fact, you’re essentially granting your customer extended payment terms. You’re shipping a large volume of product to your customer’s location and only invoicing them based on what they use in a given period. Whatever remains isn’t invoiced until the customer provides a usage report. The invoices you generate ask the customer to remit payment in 30, 45 or even 60 days. So, you’re financing the inventory far in advance of actually being paid. This is sometimes a difficult proposition for SMEs and entrepreneurs. However, when weighed against the benefit of guaranteed business, these costs are easier to accept.

2. Obsolescence

There are costs pertaining to obsolescence. If that inventory is no longer needed because it’s become obsolete, then who will cover the costs of returning that inventory to your location? Obsolete inventory often has to be scrapped entirely. At the very least, it must be discounted or liquidated. These are issues that must be addressed with your customer long before entering such an agreement.

3. Damage

If the inventory is damaged, how will you know and who will ultimately be responsible for it? You need to trust your customer to provide you with this critical piece of information. In some cases, you’ll have access to your customer’s MRP (material resource planning) or ERP (enterprise resource planning) systems and be able to see damage as it’s reported. However, if you don’t have that capability, then you’ll need to make sure you cover how damaged inventory will be handled between both parties. In most cases, damaged inventory often becomes a complete write-off. In order to avoid this issue, you should discuss proper handling and storage techniques with your customer before the inventory is shipped to their location.

4. Freight

You’ll still need to cover a cost to ship that large volume of product to your customer’s location. However, by shipping a larger volume you’ll be able to reduce your costs for each unit shipped. So, while you’ll still cover a cost of freight, that freight expense will be minimised due to the volume you’re shipping.

5. Invoicing

How will you reconcile inventory at your customer’s location? When will invoices be generated? Will an invoice be generated once the customer provides the usage report, or will those invoices only be generated at the end of a given month? You must come to an agreement as to when your customer will provide their usage report and when you’ll generate the monthly.

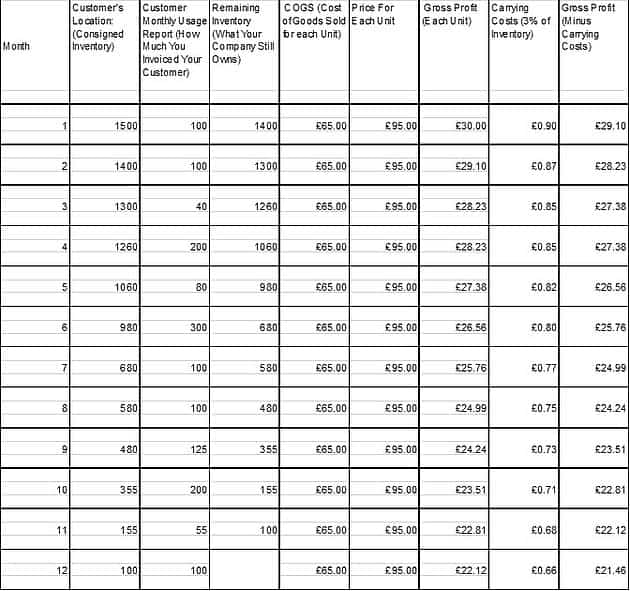

The table above is pretty straightforward. In the first month your company ships 1500 units to your customer’s location and they use 100 units in that first month. You generate an invoice for 100 units at the end of the month and the 1400 units that remain are still owned by your company. Each subsequent month your customer provides a usage report and you invoice accordingly. The inventory that remains is owned by your company.

Inventory Carrying Charges and Your Profit on Consignment Inventory

In order to give you an idea of the costs of such an agreement, I’ve outlined the gross profit per unit sold from the first month to the last. Each time, I’ve taken the gross profit per unit of that particular month and multiplied it by your company’s carrying costs of inventory, which I’ve identified as 3 percent. Every month this 3 percent is deducted from the gross profit of the previous month’s total.

When you first shipped your product to your customer’s location, your profit was £30.00 per unit. At the end of the first month you’ve covered 3 percent in carrying costs, or £0.90 per unit. This £0.90 is deducted from the £30.00 profit, giving us £29.10 as a new profit per unit at the end of the first month. You then cover another 3 percent carrying charges for the second month. This means that £0.87 is deducted in the second month from the £29.10 profit at the end of the first month. This gives us £28.23 as the next month’s gross profit per unit. Again, we multiply the 3 percent by the previous month’s gross profit and deduct it accordingly.

Please note that this 3 percent is typically what companies apply to their carrying costs of inventory. This is merely to explain that the gross profit will decrease the longer the inventory is held and not invoices. However, you’ve protected your company against losing sales to competitors, while helping your customer avoid the high costs of not having inventory when needed. Helping your customer avoid stock outs, while securing long-term business is a win-win situation for both parties involved.